Behind the Scenes: Building a Character-based Lending Fund

Authors: Caitlin Morelli, Former Director of Special Projects, Eric Horvath, Former Director of Capital Strategies

This piece was originally published to The Great Near.

CAITLIN: Last year, we saw our financial system fail people when they needed it most. Story after story emerged of businesses owned by people of color struggling to access emergency loans from banks. We need to make finance more equitable and you believe that character-based lending is one way to do this. What is it and why now?

ERIC: There’s nothing particularly innovative about character-based lending (CBL for short). Before credit scores, and really since the beginning of money lending, financiers lent out their capital on the basis of personal relationships. A borrower’s reputation was the best signal of safe repayment.

Character-based loans already exist, but banks still rely heavily on a borrower’s credit score when deciding who gets a loan and what the interest rate will be. Data shows that credit scores are not race-neutral, and lenders who don’t have a relationship with a borrower may be more likely to discriminate or misjudge someone’s character.

Imagine living in a community without a bank—more likely if you are low-income or a person of color—and needing capital for your business. You may have options nearby, but your chances of getting approved for a bank loan, or getting a rate that you can afford, are slim. Studies have also shown that banks are more likely to shut down in communities of color and that within an 8-mile radius of a recently closed branch, small business loans were 13 percent lower.

The idea for this fund came about a year ago. I’m a part of a collective of progressive lenders and allies who wrestle with increasing access to capital for BIPOC communities, but we weren’t hearing anyone talk about race or power. We felt there was so much discussion around trying non-traditional ways to lend, but too few of those ideas were becoming reality.

We started with the goal of designing a new product based on that demand and what could be additive to what’s already out there. We called a handful of lenders doing some version of alternative lending—mostly $30-40k loans that required no credit or collateral. Collectively, these institutions had deployed more than $10 million in loans they broadly defined as character-based. Most of them were raising capital at 3-5% and offering rates to borrowers at 7-9% to offset their costs.

In the communities we support at Common Future, we felt that capital at these rates would always be less than ideal for borrowers. We asked ourselves: can we put something together that goes further? We thought we could lower the rates charged to borrowers, change who refers the businesses, and integrate community insights into the loan terms. That’s when this pilot really kicked off.

CAITLIN: Character in this case is a proxy for trust, which has become a buzzword in the social sector. We often hear folks say that they are building relationships with the “people most directly impacted.” But these relationships often exist on the terms of funders who have already formed an idea that they’re seeking validation for. How do you think about this?

ERIC: Relationships drive deals, from the nonprofit to for-profit sectors. Think about affinity groups for alma maters, family relations, etc. So much of our world is driven by friendship and familiarity, which is basic human nature. But when social and financial capital are so uneven in our society, it produces a vicious cycle of inequality.

Think about venture capital. One study found that one-third of all VC investment in the U.S. can be found in twenty neighborhoods. Because VC is primarily white-led, it’s no surprise that BIPOC founders—who are not from the same zip codes or alma maters—don’t get an equitable share of investment.

Compare this to the social sector. Funders say that they “value lived experience” and “trust marginalized communities,” but they don’t often go far enough. It’s not enough to passively listen, you need the humility and boldness to act on what you hear, even when it may contradict your original plan.

If we are talking about sharing or ceding power with those closest to problems, we have to relinquish our attachment to precedent and the belief that academic exercises are more powerful than anecdotal experiences. I feel like a big part of building this fund was leaning into these beliefs.

CAITLIN: How did you think about bringing the right stakeholders to the table?

Eric: Common Future stands on two decades of relationships with local organizations that support entrepreneurs. We approached three organizations for three reasons: they are led and staffed by people of color, they support minority entrepreneurs, and they had already experimented with providing capital to their networks of businesses. They talked about these past attempts to offer loans on their own terms. Raising unrestricted capital to subsidize affordable loans proved to be extremely challenging, if not near impossible.

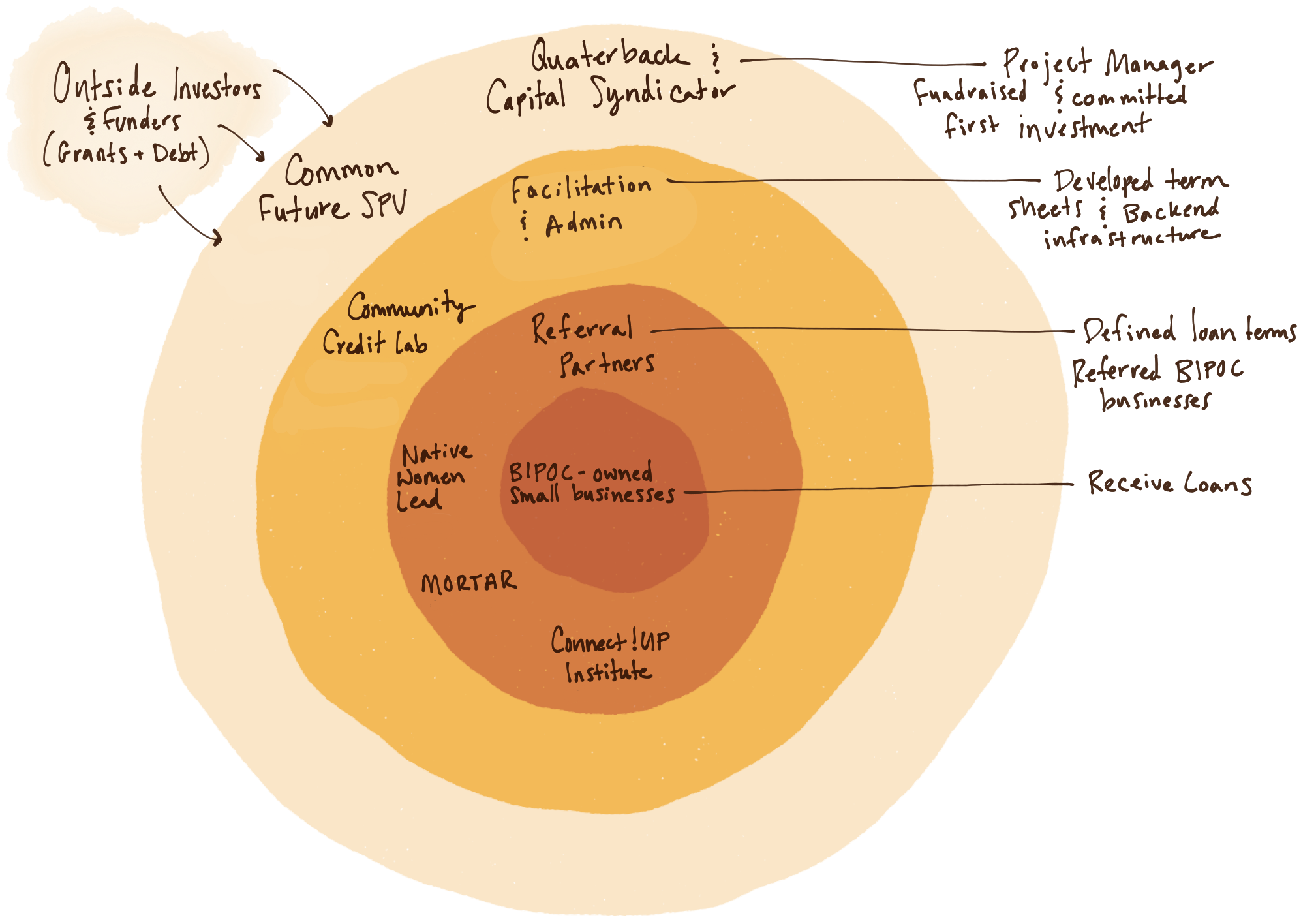

These referral partners—Allen Woods at MORTAR, Vanessa Roanhorse and Jaime Gloshay at Native Women Lead, and Elaine Rasmussen at ConnectUP! Institute—were really the drivers of the fund. Without them, we wouldn’t be here. They provided the borrower perspective that was woven into the loan terms and will be referring the applicants.

We also had conversations with Community Credit Lab (CCL) to support the back-office infrastructure that would have been cost-prohibitive to our partners. CCL believes that community partners should have the power to set criteria for investment, and this helps to center borrower needs. Most institutions in their seat might have imposed criteria that they believed would be the least risky, like requiring businesses to be profitable or have certain runway. CCL is unique in the way that they trust their community partners.

We have always believed that those who are closest to the problem must design the solution, which is part of the reason why we are constantly cultivating relationships. Without them, we believe our work would be far less impactful. Being in community with folks and developing trust is an ongoing practice that didn’t start during 2020’s protests and won’t end when the news coverage settles. It’s embedded into our DNA.

CAITLIN: Can you talk about how the partnership was structured?

ERIC: It was important that everyone felt like equals from the beginning, even if we (Common Future) played the quarterback role as project manager, lead investor, and capital syndicator. We really tried to lead with two questions: what is everyone best at and what work do we each want to grow into? Everyone had a specific role to play and trust let us thrive in our roles.

Community Credit Lab was core to the design team. They helped facilitate conversations about the loan terms with each partner and supported partners in developing Term Sheets to outline lending programs. They set up the backend software, trained the partners to use these systems, structured loan documents, and worked with our lawyers.

Common Future brought funding to the table and designed a process to evaluate the pilot’s success. The partners defined the borrower criteria (location, revenue, use of funds, target demographics) and will refer businesses in their networks that are ready to receive capital but would otherwise not get it from existing capital providers.

We also worked closely with people with technical expertise, such as Walter Alarkon, a Common Future Legal Fellow from Orrick, and Sean Campbell, a Technical Advisor to Common Future who provided insight on fund structuring from his time in finance. For anyone trying to put together something like this, I can’t recommend enough how important it is to find experienced, values-aligned partners from the onset.

My interpretation of the fund structure from Eric’s explanation.

CAITLIN: How did the topic of power come up in your conversations?

ERIC: When I think about power, I think about how it shows up in the details. We didn’t ask our partners to set meeting agendas, fundraise, write reports, or do any of the annoying stuff. Most “community-driven” processes I’ve been a part of put local leaders in the role of approving decisions as opposed to making them.

It doesn’t cut it to say “trust Black and brown women.” You have to be willing to share some of the power. I always felt like our partners were the clients—like I didn’t want to let them down. They weren’t used to this dynamic given how most funders operate. It took some time to reprogram this dynamic before they understood that they were steering the ship.

Sometimes when funders want to cede power, they think they need to do less. They walk away. As the organization with the most power in theory—we were bringing the money to the table—we knew that it wasn’t enough to sit back and listen, or worse, dictate what the partners must do. We needed to actually bring our strengths to bear and unburden our already-too-busy partners from doing unnecessary labor.

CAITLIN: Tell me more about the criteria that the partners selected for borrowers and what about these terms will make the loans more equitable.

ERIC: The beautiful thing about this fund is that ConnectUP!, MORTAR, and Native Women Lead each set their own terms. All partners plan to refer businesses that they know, trust, and have supported through their other programming for entrepreneurs, meaning they will have a track record of working together.

ConnectUP! will focus primarily on queer entrepreneurs and entrepreneurs of color that have been generating revenue for 24 months. Native Women Lead is seeking Native women entrepreneurs, and MORTAR is seeking small businesses that need funds for large capital investments, inventory purchases, or contract fulfillment. None of the partners will require credit or collateral and the average loan will be $25k with interest rates between 0-3%.

The partners had the agency to set their criteria and design their own process for approving loans. It certainly took time to get to the point where terms were clearly articulated. As new lenders, it was ingrained in us to look externally to the “experts” to define what will make a good investment. The partners had to almost unlearn this and train themselves to trust their intuition. Ultimately, we set these terms with the borrowers as the priority, not our funders.

CAITLIN: You often talk about how important it is to raise the right kind of capital to match your intended impact. In this case, it sounds like your approach to fundraising will allow you to offer affordable rates. Can you explain what this means and how you approached it?

ERIC: This was the first time that Common Future raised non-grant capital. Rather than cast a wide net, we identified the fund’s core value proposition and reached out to a small group of aligned funders and investors. This fund offers an impact-first investment opportunity that prioritizes power-building for BIPOC communities. Not everyone cares about those things or is willing to “sacrifice” financial returns, which is why we didn’t focus on those investors.

Rather than raise whatever money we could, we started with “what interest rates would be helpful to borrowers” and then worked backward. As a rule of thumb, the rate you borrow at must be cheaper than the rate that you lend at (in this case Common Future is borrowing to lend to BIPOC businesses). We didn’t want expensive capital to put pressure on the borrowers.

Put simply, imagine raising $100 and having to repay your lenders $102 in one year. If you use that $100 to offer a business a 0% loan, you’d have to figure out how to pay your lenders the $2 interest. Most often this is just charged to the borrowers. We didn’t want to pass these costs onto borrowers who have less wealth than our investors. This felt antithetical to our purpose.

One big learning is this: our fundraising hinged on the right people at the right time, as well as a targeted approach to find aligned funders. Our organization is fortunate to have a lot of reputational equity right now. The 2020 protests in the wake of George Floyd’s murder increased widespread awareness of racial injustices and demand to support BIPOC initiatives. And now, as opposed to years ago, community-centered impact investing has matured and is more ready to invest in things like this.

We recognize that it’s a privilege to have a seat at the table and to say to our funders, “this is exactly how we want to set it.” Despite these unique circumstances, we saw that impact-first investors are hungry for more opportunities. We just need to build the buckets to collect the rain.

CAITLIN: What’s the big hypothesis behind this fund? If these loans succeed, what do you hope will change in finance as a result?

ERIC: We’re betting that local leaders know where this money needs to go to best support Black, Brown, and Indigenous-owned small businesses. Vanessa, Elaine, and Allen don’t have troves of big data to prove why these borrowers are trustworthy. They do consider financial indicators, but they take a more expansive approach. To some degree, they just know. Look at venture capital, private equity, and the rest of it. So much of it is based on intuition and belief in individuals. Why can’t we believe in people of color the same way?

I hope that this helps the lending industry think differently about trust and offer more creative products that meet the needs of small businesses. It shouldn’t be surprising that Black and brown folks do not want to engage with banks after years of extractive lending, redlining, disinvestment, and bank closures in communities of color. Creativity might look like investing in, and ceding power to folks who can de-risk investments by the nature of their relationships.

I hope that CBL sparks similar initiatives so that this approach is commonly accepted in a few years. Community leaders should be able to have control over allocating more capital and there should be affordable backend infrastructure to meet their lending needs. To push the field, we’ll publish data on what works, specifically how we define trust and character.

Can lending be different? Do people need fancy training to spot credit-worthy businesses and make loans that perform? I don’t know, but I’d bet on the answer.